Why Hydrogen Engines Face a Narrowing Window of Adoption in the Commercial World

In 2025, Europe’s second-largest truck OEM, MAN Truck & Bus, will deliver 200 hydrogen trucks powered by its in-house H45 hydrogen combustion engine. These trucks will emit less than 1g of CO₂/tonne-km (drastically lower than a comparable diesel), with ranges up to 600km and 15-minute refueling. They also require no heavy and expensive lithium-ion batteries, yet according to MAN will meet the EU’s criteria for a zero-emissions vehicle. How is this achieved, and with such strong credentials, why are more in the industry not moving towards hydrogen internal combustion (H2ICE) as a zero-emissions solution?

H2ICE is fast-to-market…

As covered by IDTechEx in its in-depth review of the subject, “Hydrogen Internal Combustion Engines 2025-2045: Applications, Technologies, Market Status and Forecasts”, H2ICE is being explored as a solution for hard-to-abate transport sectors by a variety of OEMs. IDTechEx research indicates that while hydrogen chemical properties result in slightly different combustion characteristics to conventional gasoline/diesel engines, a suitable performance can be achieved with the right engine operation (lean burn spark-ignition with a λ > 2.2). Although some components (such as fuel injection and storage systems) must be redesigned, there is still significant potential for leveraging existing diesel components and production facilities. BorgWarner, a major automotive supplier, told IDTechEx at a conference, “H2 ICE is a fast-to-market powertrain solution that requires only minor adjustments to the existing internal combustion engine to meet both zero-emission CO₂ targets and future emissions regulations”.

If H2ICE offers significant emissions reductions, can be done quickly, and does not compromise on performance and range (essential metrics for commercial vehicles), then what is holding it back?

The necessary infrastructure is not ready at scale

H2ICE requires hydrogen. If well-to-wheel CO₂ emissions reductions are the goal (as opposed to just tailpipe emissions, then low-carbon blue or green hydrogen must be used. This must not only be produced (for example, through renewable electricity-powered electrolysis), but then compressed, transported, stored, and finally dispensed into the vehicle. This process costs energy, and the necessary infrastructure is almost non-existent in most regions.

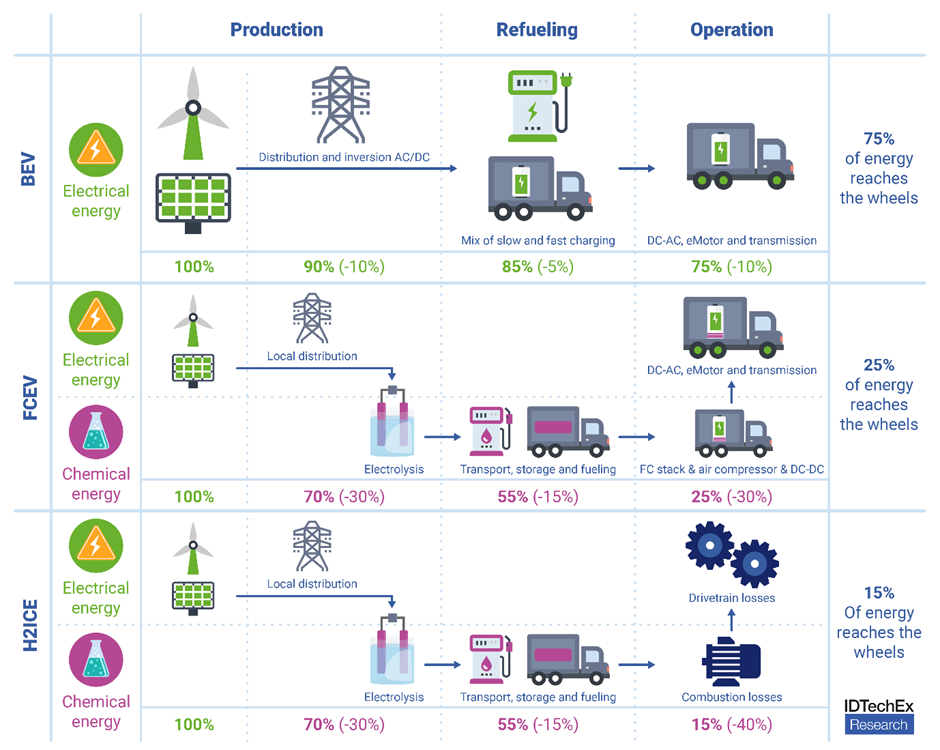

IDTechEx report examines the energetic pathways involved in BEV, FECV, and H2ICE powertrains. H2ICE has the lowest overall energy conversion rate, with extensive losses in both hydrogen production, distribution, and combustion.

As reported by IDTechEx, as of July 2024, there were 1063 hydrogen refueling stations (HRSs) globally. This compares with some 4 million EV chargers available globally in 2023, an order of magnitude larger. HRSs are also highly regionally focused, particularly in China, Korea, Japan, and California. Although the general trend has been an increase in HRSs available, this is not the case in some regions.

Germany has the largest rollout of hydrogen refueling infrastructure in Europe. The period up to 2022 saw strong growth in the number of H2 stations however, the past two years have seen stagnation at around 80 stations. Some HRS have even closed, such as the several stations Everfuel announced closing in September 2023. It cited “immature hydrogen mobility market and technology”.

California has also seen closures. In early 2024, Shell announced the permanent closure of its 5 HRS in the state. This came after earlier plans for 48 new Shell-built HRS were canceled, before 3 of the 5 stations were temporarily closed in September 2023. Finally, in February 2024, Shell announced that these closures would become permanent and apply to all of their stations, marking a major blow to the rollout of hydrogen infrastructure across the state. Shell cited “political and economic uncertainty in the initial stages of market deployment”.

Competition on the horizon

Beyond a lack of available infrastructure, H2ICE faces another threat in the form of electrification. Specifically, battery electric trucks and fuel cell electric trucks also offer zero-emissions solutions.

Much like battery electric cars, battery electric trucks run purely on electricity stored in a battery. Currently, the sheer size and cost of the battery required to provide a heavy class-8 truck with the range it requires is immense. While a car may have a battery of around 60kWh, IDTechEx research indicates some trucks are reaching 800kWh and beyond (such as the Tesla semi). Not only is this incredibly large and heavy (potentially around 4,500kg), but also expensive. With a pack price of US$200/kWh, an 800kWh pack would cost US$160,000 USD – more than a diesel truck costs! Charging is also emerging as a major issue, with a truck EV charging station requiring a huge draw from the grid to charge at MW rates.

Despite these challenges, battery electric trucks are the most efficient use of electricity, and thus bring potentially significant operation savings (with low electricity costs). Continually decreasing Li-ion battery pack prices and adopting cheaper chemistries, such as LFP, will gradually improve the capital costs of electric trucks. MW charging is emerging as a new segment of high-powered DC fast charging, and while diesel-like refueling rates are unlikely, a 45-minute charge (compatible with the legal minimum break in the EU) appears feasible.

Fuel-cell electric trucks also utilize hydrogen, but rather than burning it in an engine, it is combined with oxygen across a fuel cell membrane to produce electricity and water. One benefit of this is a generally higher efficiency level, meaning that a truck can travel further on the same amount of (expensive and hard-to-source) fuel. Fuel cell electric vehicles have been around for decades, but have struggled to take off due to the same constraints of hydrogen-related infrastructure currently facing H2ICE. However, with more efficient drivetrains, and zero tailpipe emissions (vs trace emissions for an H2ICE vehicle), IDTechEx expects fuel-cell electric trucks to be in many situations favorable to an H2ICE truck. Thus, even if the hydrogen infrastructure can be deployed at scale, H2ICE faces stiff competition from its electric counterparts.

To find out more about this IDTechEx report, including downloadable sample pages, please visit www.IDTechEx.com/H2ICE.

For the full portfolio of hydrogen market research available from IDTechEx, please see www.IDTechEx.com/Research/Hydrogen.